When Hardcore Industry Goes Consumer-Grade

Linus Torvalds wrote in Just for Fun that people go through three stages when doing things: survival, social status, and entertainment.

In Shenzhen and the Yangtze River Delta, a breed of company does something that maps precisely to the endpoint of that trajectory — collapsing industrial-grade hardcore equipment into consumer products and turning creation and manufacturing into a form of entertainment.

- DJI turned 3,000 smart flying camera

- Bambu Lab collapsed 2,000 out-of-the-box home machine

- xTool pressed 1,500 desktop format

- Hypershell took the 30 kg / 799

- Unitree replaced Boston Dynamics’ 1,600 Go2

- Xmachine took the 8,000**

Each is a two-to-three order of magnitude compression. Each was shipped by a local team in the last three to five years. Read together they offer the clearest window into how “consumer-grade downsizing” actually happens in 2020s China — not through policy, not through subsidies, but through supply chain density, engineer cost structure, iteration speed, and go-to-market capability on overseas markets.

I. What “Consumer-Grade Downsizing” Means

Not every move from industry to consumer qualifies as consumer-grade downsizing in the sense I’m using. The stricter pattern requires three conditions simultaneously:

1. Two-to-three orders of magnitude of price compression. Not a discount — a collapse of factory-floor equipment into a price an individual can afford. Drones from 3K. CNC from 8K. Robot dogs from 1,600. All are 50× or more compressions.

2. Out-of-the-box. Industrial equipment requires more than money — it needs calibration, tuning, operators, site preparation. Consumer-grade downsizing has to eliminate that layer. Unbox, install software, press a button. Bambu Lab’s single biggest improvement over open-source RepRap-family 3D printers is this shift from “engineer’s toy” to “appliance.”

3. Home-friendly form factor. It has to fit in a study or garage, not a workshop. Xmachine XM-100 only makes sense as “desktop five-axis CNC” because it is actually desktop. A factory mill crammed into a basement is not downsizing.

Use these three conditions as the bar and the story below examines six canonical cases — DJI, Bambu, xTool, Hypershell, Unitree, Xmachine — plus several “other species” on adjacent paths.

II. From the Battlefield to the Desktop

Drones, 3D printing, CNC — all three trace their origins to the same place: military and defense.

Drones: The modern drone was born on the battlefields of World War I in 1917. Britain built the “Aerial Target”; the US secretly developed the “Kettering Bug” — an aerial torpedo made of wood and cardboard. In 1935, the Royal Navy created the recoverable “Queen Bee,” and in its honor radio-controlled aircraft were named “Drones.” During the Cold War, drones served as unmanned U-2 stand-ins. Post-2001, Predator made the leap from ISR platform to strike platform over Afghanistan. Before 2005, consumer drones effectively didn’t exist.

3D Printing: Born in early-1980s laboratories. In 1984, Chuck Hull invented Stereolithography (SLA) and patented it — not to make toys, but so automotive and aerospace engineers could get complex plastic prototypes in days instead of months. Stratasys then developed FDM, with the US military and NASA as its first customers. The 2009 expiry of the FDM core patent opened the door for RepRap and the early Creality / MakerBot wave to bring the technology to consumers.

CNC: Born in the late 1940s during the early Cold War. The US Air Force discovered that traditional machine tools couldn’t handle the complex curved surfaces of helicopter rotors. John Parsons proposed controlling machines with punched cards. In 1952, MIT, funded by the US military, built the world’s first numerically controlled machine tool — a monster that filled an entire room. Five-axis CNC technology is still on the U.S. export control list.

Laser cutters: 1960s lab, 1970s military (missile casing cutting), 1980s factory, 2000s hobbyist.

Exoskeletons: 1960s GE Hardiman (military lifting), 1990s medical rehab, 2000s US HULC program, 2020s consumer hiking variants.

Robot arms: 1961 Unimate on GM production lines, 1980s factory standard, 2010s UR / ABB cobots, 2020s desktop education units.

Consistent pattern: from battlefield to factory to desktop. Technology matures → patents expire or diffuse → supply chain matures → consumer players appear. Each step takes roughly 20 years.

III. DJI: The Bellwether of Consumer-Grade Downsizing

DJI is the earliest, fullest demonstration of this pattern — how far consumer-grade downsizing can go was validated by DJI first.

Frank Wang founded DJI at HKUST in 2006. The 2013 Phantom made the consumer drone an assembled product, not a kit. The 2016 Mavic Pro folded the four-rotor form into a backpack-scale package at $999. Every generation of Mavic / Air / Mini / Avata since repeats the same move: shrink the form factor, hold the image quality, lower the skill floor.

DJI in 2024-2025 (public data):

- 75-85% global market share in consumer drones

- Valued by outside estimates in the $16-20 billion range (private)

- 2024 consumer drone market ~$11 billion worldwide; DJI derives 60%+ revenue from the consumer segment

- In 2025, FCC national-security restrictions began limiting U.S. sales of newer models like Mavic 4 Pro and Mini 5 Pro — an external pressure that, if anything, confirms the extent of DJI’s position

- Growth of roughly +35% YoY in 2024 (third-party estimates)

Why DJI wins, structurally:

- Vertical integration: gimbal motors, IMU, GPS modules, video transmission protocols — all in-house. Competitors (3DR, Parrot, GoPro Karma) who relied on external component suppliers couldn’t match DJI’s iteration speed.

- Shenzhen supply chain: drones share ~99% of upstream components with phones and cameras. DJI can spin a new generation in 12-18 months.

- Ocean-sky strategy: establish consumer + imaging first, use scale to enter industrial verticals (agriculture, utilities, surveying), then circle back to global markets. Most Boston/Silicon Valley robotics companies do this in the opposite order.

DJI’s significance: it proved that consumer-grade downsizing is commercially viable at scale. Every later case references DJI’s path.

IV. Bambu Lab: DJI Veterans Take On 3D Printing

November 2020: Shenzhen Bambu Lab is founded. The five founders — Tao Ye (CEO), Gao Xiufeng, Liu Huaiyu, Chen Zihan, Wu Wei — all came from DJI.

That fact is the most important signal. After DJI conquered consumer drones, a cohort of engineers with a full engineering-scale tour of duty left and re-applied the same method to another “not-yet-conquered” hardware category. They picked 3D printing.

July 2022: Bambu’s Kickstarter for the X1 Carbon hit 7M. Priced at $1,199. Against contemporary Creality lines, the X1 Carbon delivered:

- CoreXY architecture + 500 mm/s print speed (typical machines at the time: 100 mm/s)

- Full auto-calibration (bed leveling, nozzle offset, vibration compensation) — from unboxing to first print in 15 minutes

- Multi-color printing (AMS system, up to 16 colors)

- App-based remote monitoring + lidar print-quality inspection

2023 brought the P1 series (799). 2024 brought A1 / A1 mini (599), pricing into Creality’s base range.

Bambu Lab 2024-2025 metrics:

- 2024 revenue

6 billion RMB ($830 million US dollars) - 2024 shipments ~1.2 million units

- From zero to $1B+ annual revenue in three years

- 29% global share of consumer 3D printers in 2024

- In the first three quarters of 2025, 37% share of the global sub-$2,500 entry segment — overtaking Creality

- Valuation over $3 billion (Tencent among 2024 investors)

Bambu Lab is a nearly verbatim application of the DJI method to a new category: vertical integration + out-of-the-box + rapid iteration + Shenzhen supply chain. By 2025 it became the second consumer-hardware brand to approach monopoly status in its segment.

V. xTool: 47% Overseas Share in Consumer Laser Engravers

xTool is the consumer laser engraving / cutting brand that spun out of Shenzhen-based Makeblock in 2019. Its products look like a closed desktop version of a factory CO₂ laser cutter — because that’s exactly what they are. It compresses 50,000 factory laser equipment into a 2,699 desktop machine.

xTool in 2024-2025:

- Q1-Q3 2025 global GMV share in laser engraving / cutting: 47%, roughly 6× the #2 brand

- Global personal creative tools GMV share: ~37%

- Price range 2,699 core; flagship xTool P2 (55W CO₂) at $4,399

- Filing for a Hong Kong IPO (early 2026), positioned as “the first listed consumer laser engraver company”

- Investors: Tencent, Sequoia; founder came from Anker

How does it get to 47%?

- Overseas-first strategy: xTool targeted the U.S. + EU maker culture where the spending and community already existed, avoiding China’s relatively small hobby market

- Full product line: from entry-level diode (1,000) to professional CO₂ ($4,000+)

- Content marketing: “Gift-making with xTool” / “side hustle” YouTube videos hit scale

- Compression vs industrial equipment: factory CO₂ cutters are 100-500W, workshop-scale, 100,000. xTool P2 is 55W CO₂ in a closed ~5kg desktop machine for $4,399 — collapsing the operating, safety, and siting barriers in one stroke

Global laser tools market is projected to grow from 39.1B in 2030 (33.8% CAGR). xTool is positioned in the consumer tier — the fastest-growing band.

VI. Hypershell: The Consumer Exoskeleton Unicorn

Exoskeletons are the textbook “battlefield → hospital → desktop” species. Military HULC (soldier load assist) and severe-rehab medical exoskeletons are both 30-40 kg devices with external power supplies and $50K+ price tags.

Hypershell was founded in Shenzhen in 2022 by Sun Kuan (a post-90s engineer with robotics hardware + exoskeleton research background). The positioning is sharp — outdoor hiking and everyday assistance.

Product line:

- Hypershell Go X: entry level, 2 kg, 15 km range, $799

- Hypershell Pro X: mid-tier

- Hypershell Ultra: flagship $1,799, IFA 2025 Best Innovation Award, the world’s first SGS-certified consumer exoskeleton

Downsizing compared to industrial / medical exoskeletons:

| Dimension | Military / medical | Hypershell |

|---|---|---|

| Weight | 20-40 kg | 2 kg |

| Range | External power / 1-2 h | 15 km / several hours |

| Price | 80,000 | 1,799 |

| Use case | Military / rehab | Hiking / daily / elderly assist |

2025 data:

- Closed 400M

- Investors: Guanghe Capital and 5Y Capital co-led; Meituan Dragonball and Monolith participated

- Sales channels in 70+ countries, cumulative shipments in the tens of thousands

- Kickstarter crowdfund: 2,600 backers, $1.2M+, 3,000 units

Hypershell took a category that “feels like 2040” and put it in stores in 2025. It is also the first consumer wearable robotics brand to reach unicorn-adjacent valuation.

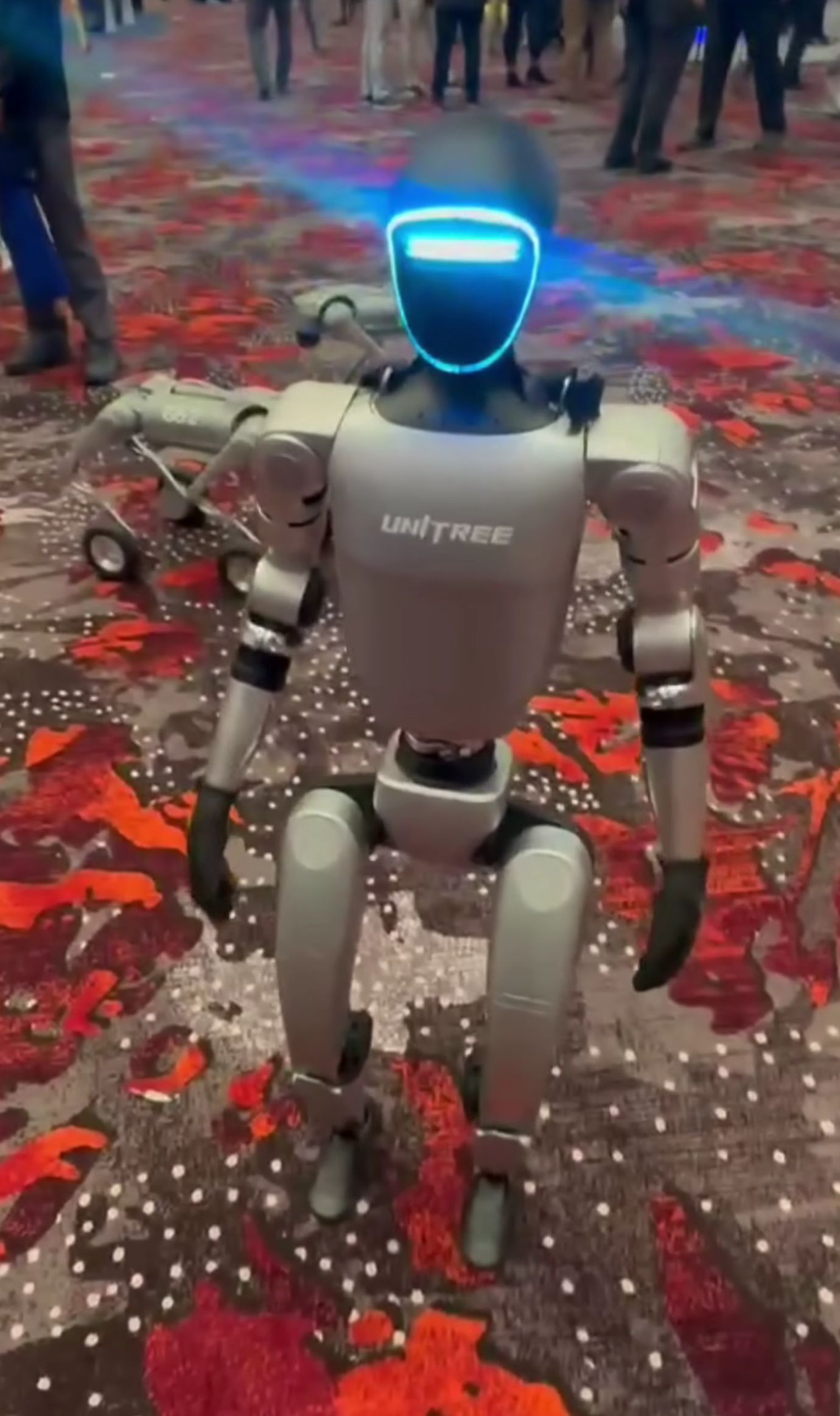

VII. Unitree: Undercutting Spot by 50×

Unitree Robotics was founded in Hangzhou in 2016 by Wang Xingxing. It isn’t in Shenzhen, but the Yangtze River Delta industrial belt shares the same ecosystem. Unitree’s main lines are quadruped robots and humanoid robots — the two most dramatic downsizing stories in robotics.

Quadruped robot comparison:

| Product | Price | Note |

|---|---|---|

| Boston Dynamics Spot (industrial) | ~$75,000 | Launched 2020, used for military/police and industrial inspection |

| ANYmal (industrial) | ~$150,000 | ETH spin-off, oil & gas |

| Unitree Go2 Air | $1,600 | 2023 launch, consumer / education |

| Unitree Go2 Pro | $2,800 | Added LiDAR, upgraded battery |

| Unitree Go2 EDU+ | $13,250 | Research / development variant |

An order of magnitude compression: Go2 undercuts Spot by roughly 50× while preserving quadrupedal gait, dynamic balance, SLAM, and AI perception. IEEE Spectrum’s 2023 review used the phrase “surprisingly competitive.”

Humanoid robot comparison:

| Product | Price | Note |

|---|---|---|

| Boston Dynamics Atlas (research) | Not for sale | 2013 DARPA project, no commercial path |

| Tesla Optimus Gen 2 (est.) | ~$20,000-30,000 | Small-scale delivery in 2025 |

| Figure 02 / Agility Digit | ~$50,000-100,000 | Warehouse / research |

| Unitree G1 | $13,500 | 2024 launch, consumer / research |

At launch in late 2024, the G1 was the first humanoid robot with real locomotion at a price under $15,000 — again a 5× to 10× compression versus Figure / Agility / Optimus.

Unitree’s path mirrors DJI and Bambu: vertical integration of motors, reducers, control boards, rapid iteration, and a Yangtze-Delta manufacturing base. Boston Dynamics, who started at roughly the same time as Unitree’s older hardware, remains a research and engineering icon with virtually zero consumer market presence.

VIII. Xmachine: Desktop Five-Axis CNC

The five previous cases have several years of market validation. Xmachine is the newest wave (2025-2026) of consumer-grade downsizing.

Product: Xmachine XM-100, a desktop five-axis machining center — the world’s first desktop-class true five-axis CNC.

Specs:

- In-house five-axis linkage CNC control (RTCP true five-axis)

- Spindle at 18,000 rpm (high-speed permanent-magnet synchronous motor)

- Precision sensing + wireless workpiece positioning

- Footprint similar to a desktop tower PC

- Retail price: 58,000 RMB (~$8,000)

Downsizing comparison:

| Category | Price | Size |

|---|---|---|

| Industrial five-axis CNC (Fanuc / DMG MORI) | 3,000,000+ | Shop-floor, tons |

| Professional five-axis (Haas UMC) | 200,000 | Small shop |

| Desktop three-axis (Carbide 3D, Bantam) | 10,000 | Desktop |

| Xmachine XM-100 (desktop five-axis) | $8,000 | Desktop, home-friendly |

Why five-axis matters: three-axis CNC can only cut “up-and-down” surfaces. Anything with complex curvature — turbine blades, aerospace structural parts, molds — needs five-axis. Five-axis linkage control was industrial-only, and still on the U.S. export control list. Xmachine compressed that capability into a desktop form factor at consumer pricing. It is the most extreme case in the last five years.

Market validation: on overseas crowdfunding platforms in early 2026, Xmachine exceeded its funding goal by 102×. That’s not final sales but it reflects immediate acceptance of “desktop five-axis CNC” as a category by the global maker community.

Limits: compared with factory five-axis, XM-100’s working travel (~200 mm range), spindle power (~500W), and rigidity are orders of magnitude smaller. But for consumer users — designers, jewelers, dental technicians, small home workshops — it does what only factories used to.

IX. Other Species

Consumer-grade downsizing in 2020s China is a genre, not just six brands. Some parallel paths worth naming:

Robot arms: industrial six-axis arms (Kuka, ABB) cost ¥300K-800K and occupy a floor. After 2020, DOBOT, Elephant Robotics, Unitree pushed desktop six-axis arms down to ¥10K-30K. Typical use: auto-filming, STEAM education, small production lines, even latte art. The key technology compression was harmonic reducers — Japanese and German parts with <1 arc-min precision got domestic substitutes (Suzhou Lvde, Laifu), driving prices down sharply.

AR / AI glasses: traditional HMDs were military pilot and industrial CAD review hardware at tens of thousands to hundreds of thousands of dollars. Rokid Glasses (mass production in late 2025) put an AI-enabled AR glasses product at ¥2,499 using Qualcomm Snapdragon AR1. Preorders passed 500,000 units by year-end 2025. Xreal, Pimax, TCL RayNeo are in the same race.

Thermal imaging: once tank night-vision, missile IR guidance, and national grid inspection equipment at hundreds of thousands of RMB. InfiRay, HIKMICRO (Hikvision’s consumer brand), Seek Thermal turned it into phone-plug-in and outdoor gear — floor heating leak detection, wildlife spotting while camping, photography in total darkness. 2024 global thermal market ~$7B; Chinese players are gaining share rapidly.

Bench test instruments: oscilloscopes, multimeters, function generators — once the exclusive domain of Tektronix, Keysight, and other US-Japan industrial brands, with entry models starting at $10K+. UNI-T, OWON, Rigol, Siglent brought digital oscilloscopes down to ¥1,500-5,000 with 100-200 MHz bandwidth catching up to professional tier. For individual electronics hobbyists, hardware startups, and university labs, this is a 10× compression.

Smart soldering stations: traditional high-end stations (Hakko, Weller) are 70-100** with OLED display, temperature curves, OTA firmware. Hobbyists replaced their legacy stations almost wholesale.

Desktop vacuum equipment, desktop SEM electron microscopes, desktop CT — the same pattern is starting to emerge across category after category.

X. Market Tiers: Industrial, Professional, Consumer

Split the market into three tiers and the same product category has very different price points, customers, moats, and competitive dynamics across them. The table below extends the tier comparison beyond drones, 3D printers, and CNC:

| Category | Consumer (size / price / leaders) | Professional (size / price / leaders) | Industrial (size / price / leaders) |

|---|---|---|---|

| 3D Printing | ~200-1,500 / Bambu Lab, Creality | ~3,000-15,000 / Raise3D, Formlabs | ~100K-$2M+ / Bright Laser Tech, EOS, Stratasys |

| Drones | ~300-2,500 / DJI, HoverAir | ~5,000-35,000 / DJI Enterprise, XAG | 100K-$10M+ / Northrop Grumman, EHang, AVIC |

| CNC | ~300-10,000 / Carbide, Genmitsu, Xmachine | ~10K-150K / Haas, Tormach | 150K-$3M+ / Fanuc, DMG MORI |

| Laser cutting / engraving | ~300-5,000 / xTool, WAINLUX, LaserPecker | ~10K-100K / Epilog, Trotec | 150K-$2M+ / TRUMPF, Han’s Laser |

| Quadruped robots | Emerging (<1,600-5,000 / Unitree | ~5K-30K / Unitree, ANYbotics | ~75K-200K+ / Boston Dynamics, ANYbotics |

| Humanoid robots | Emerging / $13,500 / Unitree G1 | Emerging / $20K-50K / Figure, Agility, Optimus | Early research / $100K+ / Boston Dynamics Atlas |

| Exoskeletons | Emerging (<799-1,999 / Hypershell | ~5K-30K / ReWalk, Ekso | ~30K-80K+ / Military HULC-family |

| Robot arms | ~500-30,000 / DOBOT, Elephant, Unitree | ~10K-80K / Universal Robots (cobot) | 30K-200K+ / Fanuc, Kuka, ABB |

| Thermal imaging | ~200-3,000 / InfiRay, HIKMICRO | ~3K-30K / FLIR, Fluke | ~30K-500K+ / L3Harris, FLIR |

| AR glasses | Emerging (<300-2,500 / Rokid, Xreal, Meta | ~3K-10K / Magic Leap, HoloLens | ~20K+ / Military HUD, AR IVAS |

| Bench oscilloscopes | ~300-5,000 / UNI-T, Rigol, Siglent | ~5K-50K / Tektronix, Keysight mid-tier | ~50K-500K+ / Tektronix / Keysight high-end |

Structural observations:

- The consumer tier is always the smallest (usually 5-15% of total market), but grows fastest and most often produces winner-takes-all dynamics. DJI, Bambu, xTool are all textbook examples.

- The industrial tier is the largest and most defensible (materials, certifications, customer relationships) — consumer brands rarely touch it.

- The professional tier is the squeezed middle — consumer can’t afford the R&D, industrial can’t justify the volume. 2020s middle-tier leaders (Formlabs, Raise3D) are most vulnerable.

- Direction of travel: consumer brands usually grow upward into professional, not downward from industrial. Industrial iteration rhythms don’t compress well to consumer cadence.

XI. Why Shenzhen (and the Yangtze River Delta)

Five of six cases are from Shenzhen (DJI, Bambu, xTool, Hypershell, Xmachine); the sixth (Unitree) is from Hangzhou. Not a coincidence. Consumer-grade downsizing needs four things that exist together in these two regions:

1. Supply chain density. Within 50 km of Shenzhen and 300 km of the Yangtze River Delta, the upstream suppliers for phones, cameras, home appliances, cars, toys, and medical electronics are all co-located. Drone design uses IMUs, motors, ESCs, video links, camera modules that share ~95% of the supply chain with phones and cameras. Shenzhen can prototype in 2 weeks, trial-produce in 4 weeks, mass-produce in 12 weeks. Boston-area supply response times for similar products are 6-12 months.

2. Engineer cost structure. A similarly experienced hardware engineer costs roughly ¥300K-800K (200K-400K in Silicon Valley. Hardware product iteration requires lots of circuit + mechanical + firmware + algorithm engineers — a density × speed curve where Shenzhen has an order-of-magnitude cost advantage.

3. Iteration speed. A typical Shenzhen hardware startup’s product iteration cycle is 3-6 months (software update + minor hardware), with major revisions every 12 months. The Western equivalent is 18-24 months. For “compress industrial to consumer” problems, fast iteration is the only path — get it wrong once, fix it; convergence needs three tries at most.

4. Overseas go-to-market capability. Since 2018, Shenzhen hardware teams have collectively mastered “Amazon + independent site + Kickstarter + YouTube influencer” go-to-market combinations. xTool, Hypershell, Bambu Lab are all overseas-first, domestic-later. Five years ago only Anker did this. Today dozens of companies run the same playbook.

Stack these four factors and Shenzhen + Yangtze River Delta is 3-5× more efficient at hardware iteration startups than other regions. This is not an industrial policy outcome — it’s a self-organized industrial ecosystem built over three decades, from 1990s Pearl River Delta OEM, through 2000s “Shanzhai” phone-building, through the 2010s Maker movement, up to today.

XII. Common Patterns

Six cases plus the other species reveal five shared characteristics of successful consumer-grade downsizing:

1. Teams from the “prior generation’s winners”. Bambu Lab came from DJI, xTool’s founder came from Anker, Hypershell from robotics. Without the prior experience of shipping a consumer hardware product at scale, 90% of attempted downsizing dies before product-market fit.

2. Overseas first, domestic second. Kickstarter → Amazon → independent store → brand. Overseas users have higher willingness to pay for new hardware categories and stronger content amplification, while bypassing the relatively modest Chinese hobby market ceiling.

3. Vertical integration + Shenzhen supply chain. Key components built in-house (control boards, motors, algorithms), peripherals use standard supply chain parts. This combo lets a small team ship a hardware product in 12 months — impossible elsewhere.

4. Out-of-the-box + software experience. Half of “hardware becoming consumer” is the software experience becoming consumer. DJI’s Fly app, Bambu’s Bambu Studio, Unitree’s phone control — these “non-hardware” parts determine whether non-engineer users will accept the product.

5. Brand = category. The endpoint of consumer-grade downsizing is a brand that owns a category. DJI = drone, Bambu = 3D printer, xTool = laser engraver, Hypershell = exoskeleton, Unitree = robot dog. Once that happens, latecomers (Creality, Ortur) face an asymmetric battle.

XIII. Looking Forward

Pull all six cases together and you see something that matters — consumer-grade downsizing in 2020s China has become a repeatable methodology.

Input: a team with prior hardware engineering experience + Shenzhen or YRD supply chain + overseas go-to-market + a “hardcore category that hasn’t yet been consumer-ized.”

Output: a brand that in three years goes from zero to $1B+ in annual revenue, 30%+ global market share, and brand-equals-category recognition.

DJI ran this playbook the first time in 2013. Bambu Lab ran it a second time in 2022. xTool, Hypershell, Unitree, Xmachine are running their own iterations in 2024-2026.

Looking ahead, too many hardcore categories are still waiting to be downsized: consumer SEM electron microscopes, consumer mass spectrometers, consumer cryo-EM, consumer precision assembly robots, consumer prosthetics, consumer BCI (brain-computer interfaces) — every item today priced in the hundreds of thousands to millions in factory or lab equipment could see a Shenzhen or Hangzhou version of “2 kg / $799 / out-of-the-box” within ten years.

This isn’t a story about “Chinese manufacturing being cheap.” It’s a story about engineering capability evolving into a new species inside a specific geographic and industrial ecosystem — exactly the path Linus Torvalds described, from survival to social status to entertainment, for humans and for industry alike.

References

DJI:

- DJI corporate site / DJI Enterprise

- Runwise: How DJI captured 72% of the global drone market through vertical integration and rapid iteration

- Tencent News: What lets DJI dominate the global drone market

- Sina Finance: One-day deep dive on DJI Innovation

- Qianzhan Research: 2024 China drone industry competitive landscape

Bambu Lab:

- Bambu Lab corporate site

- Wikipedia: Bambu Lab

- EqualOcean: Bambu Lab nears CNY 1.5B in annual revenue

- 3DPrint.com: Billion Dollar Bambu and a New Worldview

- Tom’s Hardware: Bambu Lab overtakes Creality as the world’s top-selling budget 3D printer brand

- 36kr EN: Tencent vs DJI — Head-to-Head Battle in 3D Printing

xTool:

- xTool corporate site

- Sina Finance: Tencent and Sequoia back xTool’s bid for the “first consumer laser engraver IPO”

- Brandark: Single-product presale over $10M, laser engravers a hit overseas

- 52by: How xTool sells laser engravers to a million households

- Let’s Chuhai: Former Anker exec starts up, targeting a “niche” laser cutter

Hypershell:

- Hypershell corporate site

- Sina Finance: Hypershell closes $70M Pre-B and B rounds

- Eastmoney: Valuation near $400M, leading a new era of consumer exoskeletons

- GeekPark: Westerners snapping up the $999 Chinese consumer exoskeleton

- BrandStar: Consumer exoskeleton brand Hypershell closes multimillion-dollar Pre-A

Unitree:

- Unitree corporate site / Unitree Shop

- IEEE Spectrum: Unitree’s New Go2 Is One Dynamic Quadruped

- Unitree G1 product page

- New Atlas: Unitree Go2 Pro review

Xmachine:

- Xmachine / Xhorse3D product page

- Tencent News: Chinese desktop mills blow up overseas crowdfunding — the next Bambu Lab?

- Shenshan Xianshi: Xmachine XM-100 desktop five-axis CNC review

Other species:

- Rokid corporate site / NetEase: World’s first consumer AI+AR glasses — Rokid Glasses hits production

- InfiRay corporate site / HIKMICRO corporate site

- Technology Networks: China Consolidates Its Presence in Thermal Imaging

- DOBOT / Elephant Robotics

- Miniware / Rigol / UNI-T

Industry background:

- Torvalds, Linus (2001). Just for Fun: The Story of an Accidental Revolutionary

- Infoobs: China is the largest source of drone technology globally

- Dikongjie: 2024 Global Top 100 Drone Companies

- Fortune Business Insights: Thermal Imaging Market

- Mordor Intelligence: IR and Thermal Imaging Systems Market